According to the Federal Reserve, we continue to see tightening credit standards and declining credit quality. Lenders are also being more selective. Nearly 60% of businesses applied for some form of financing within the past year, but less than half got the full amount they requested.

Debt is increasing as well, at the same time that cash-on-hand is decreasing, where 39% of firms now carry more than $100,000 in debt, higher than pre-pandemic levels. Nearly 40% of SMBs report having less than one month’s worth of operating expenses on hand.

For businesses looking for loans, evaluating suppliers and partners, or extending credit, getting verifiable credit information has become more important than ever. In this guide, we’ll explain how businesses, lenders, and vendors can access business credit reports, how company credit checks work, the ways business credit bureaus differ, and how to interpret corporate credit reports to make smarter decisions.

What Is a Business Credit Report?

A business credit report is a consolidated record of a company’s credit-related behavior, financial risk indicators, and public record. It is designed to help assess how reliably a business meets its financial obligations over time.

Unlike a credit score, which reduces risk into a single predictive number, a credit report provides the underlying context. It shows payment behavior, adverse events, and trends, which explain why a score exists in the first place.

Business credit reports also differ fundamentally from personal credit reports. They are tied to legal business entities, rely heavily on commercial trade data, and are interpreted through a risk management lens rather than a consumer lending framework.

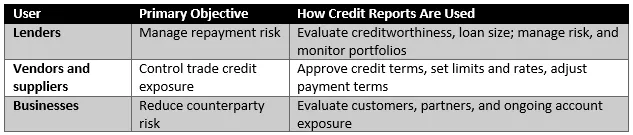

Who Uses Corporate Credit Reports?

Business credit reports support different decisions depending on who is reviewing them. While the data may be similar, the objectives and interpretation will vary depending on use.

When you pull a credit report for a company from one of the major business credit bureaus, you get standardized data that helps you evaluate them against industry norms and against your current risk threshold.

How a Business Credit Agency Operates

A business credit agency collects and organizes commercial credit data from lenders, suppliers, public records, and other reporting sources. Each bureau operates independently and uses slightly different sources. So, information from one business credit report service might look different from another agency.

One bureau may reflect deeper trade payment history, while another may surface delinquency or legal risk more quickly. Depending on the level of risk involved, it often makes sense to do a company credit check using multiple credit bureaus for a more comprehensive picture.

What Information Is Used to Build a Business Credit Report for a Company

Business credit bureaus pull together data from a variety of sources, creating a standardized and structure view of financial health. While each agency has its own way of sorting and assessing data, here’s the type of information you generally receive:

- Business identification data: Legal name, addresses, and corporate structure

- Trade payment activity: Supplier-reported payment behavior that reflects early, on-time, or late payments.

- Credit scores and risk indicators: Predictive metrics designed to assess the likelihood of delinquency or late payment.

- Public records and legal events: Liens, judgments, bankruptcies, and other filings, that may signal financial stress.

- Collections and delinquencies: Unresolved payment obligations escalated beyond standard billing.

Each category contributes a different risk signal, allowing you to make your own credit decision with verifiable information rather than relying on credit apps where businesses self-report.

How to Check Company Credit

A company credit check requires accurate business identification. You need the correct legal name of the business to make sure you get the right information. Unlike consumer credit checks where you need explicit consent, you do not need consent to pull business credit.

You have several options when it comes to company credit checks. You can sign up for subscription services at each of the credit bureaus or use a business credit report service like Command Credit. Command Credit lets you pull one or multiple business credit reports in one place. You simply enter the business name, payment information, and select the reports you want to pull. You can instantly download them for review.

On-Demand vs Subscription-Based Business Credit Report Access

Traditional access to business credit reports often required long-term subscriptions with individual bureaus. This model might work for companies that pull a significant amount of reports on a regular basis but likely doesn’t fit businesses that don’t need access to credit reporting daily. You can wind up overpaying, especially if you need information from multiple agencies. And, you have to use a separate system with each agency.

By comparison, an on-demand business credit report service like Command Credit lets you pay as you go and make sure what you’re spending exactly matches your needs.

How to Interpret a Corporate Credit Report

Interpreting a corporate credit report starts with the overall credit score as a general indicator. One of the benefits of business credit reports, however, is that you also get to see some of the underlying data that was used to come up with the score. Payment history, public records, and recent activity provide more context to help you make better decisions.

Keep in mind that a credit score is a snapshot in time. In business, things can change quickly. So, watching trends is important. Even if a credit score is within your acceptable range, a significant drop might require a closer look. Maybe someone’s always paid their bills on time, resulting in a decent credit score, but they’ve started missing payment dates lately. This might indicate there’s a deteriorating financial situation.

On the other hand, a business that has a medium-risk score that shows a strong payment behavior over the past few years might give you more confidence when extending credit.

On-Demand Business Credit Reports: Step-by-Step

Getting on-demand business credit reports is easiest when you treat it as a repeatable workflow. These steps are designed to help lenders, suppliers, and businesses run consistent checks, pull the right corporate credit reports at the right time, and document decisions in a way that holds up internally.

Step 1: Define the Decision and the Exposure You Are Evaluating

A credit check for a small trade line is not the same as underwriting a loan, approving net terms for a high-volume buyer, or evaluating a long-term partner. So, you’ll want to think in terms of exposure and what information you’ll need to make the best decision about credit approvals or terms.

Step 2: Collect the Business Identifiers Needed for an Accurate Match

While you don’t need explicit permission to check company credit, you do need the correct legal name. If you use a credit application, you can ask for it there. Regardless, you’ll need to know the legal business name, which can be different from their DBA name or brand name. You’ll also want a current business address.

A phone number and website address can be helpful for verification while an Employer Identification Number (EIN) can make verification easier.

Step 3: Decide Which Bureau Perspective You Need, and Whether You Should Cross-Check

For low exposure decisions, you may only need one report. For high exposure, longer terms, or new relationships, it is often a good idea to check company credit at multiple agencies.

A simple way to decide:

- Use a single report when there’s low risk or limited exposure.

- Use multiple reports when exposure is material, the business is new to you, or the decision has longer-term consequences.

If you’re unsure which way to go, you can get in touch with one of our business credit experts at Command Credit, and we’ll help you figure out the best approach for you.

Step 4: Pull the Business Credit Report on Demand

Pulling a credit report for a company takes only a few steps with Command Credit:

- Enter the business identification information.

- Choose the type of report or corporate credit reports you want.

- Enter your payment information.

- Instantly download your company credit check.

Step 5: Validate You Are Reviewing the Correct File

Check the business name formatting, address history, and industry classification (if shown) included in the file. If anything looks inconsistent, you’ll want to double-check. Making credit decisions based on a different company’s information can put you at risk.

Step 6: Review the Score and Evaluate Supporting Data

The overall credit score is a good indicator, but it’s not everything you want to look at. Often, you’ll find significant information within the supporting data, such as:

- Trade payment patterns and terms

- Recency and frequency of late payments

- Collections or delinquency signals

- Public records or legal events

This is where credit decisions become defensible. A score without context is easy to misinterpret, but the details help round out the story.

Step 7: Evaluate Trend Direction and Recency

For risk assessment, direction matters. Even your best companies or long-term industry leaders can run into problems. So, a credit score built on decades of on-time payments might remain high while a run of late pays or recent defaults can indicate signs of financial distress.

If you are making long-term (or large-scale) decisions, you might want to pull business credit reports at certain milestones to make sure things haven’t changed. For example, during contract renewals, new credit requests, limit increases, or contract expansions.

Step 8: Align your Decision with Your Use

While each of the credit bureaus will rank businesses based on their credit scores, indicating low, medium or high risk, your approval likely requires more, depending on broad categories. Every credit decision is viewed in terms of your overall exposure, your risk tolerance, and your business needs.

For example, for trade credit, the most important indicator is likely payment behavior. Is the customer paying other creditors consistently on time? For suppliers or partners, you’ll want to look for signs of financial stability, and an absence of adverse events like liens, judgments, or bankruptcies.

Step 9: Document the Decision and Evidence

You’ll want to document your decision and the underlying data you used to make that decision. This is critical for internal accountability and to defend yourself in case of claims or legal proceedings. While you should talk to your business counsel for a legal opinion, generally the information you’ll want to keep includes:

- Date/time the report was pulled

- Which bureau reports were reviewed

- Key score(s) and trend direction

- Primary risk drivers (positive and negative)

- Decision outcome (approve, decline, adjust terms, request additional review)

Depending on industry and use, there may be other legal requirements. Overall, consistent credit policy enforcement is key to avoiding conflicts, so keeping the information on hand can help in case any questions are raised.

Consider Ongoing Credit Monitoring

On-demand company credit checks are great tools when you’re onboarding new clients or conducting periodic reviews. However, you may also benefit from ongoing account monitoring to be on the lookout for changes in financial health. The sooner you know there are troubling signs, the sooner you can act to protect your bottom line.

Many companies also choose to include portfolio scoring with a business credit report service. Command Credit provide portfolio scoring and analysis to help you determine a baseline for risk tolerance and review your current policies to help you find exposure.

FAQs—Frequently Asked Questions About Corporate Credit Reports

How do I get a business credit report? You can do a company credit check on demand, through Command Credit, from Equifax, Experian, Dun & Bradstreet, or Credit Reports World and download it instantly.

What makes up a small business credit report? A small business credit report typically includes business identification data, trade payment history, credit scores and risk indicators, public records, and any collections activity.

How do I establish business credit? Business credit is established by forming a legal business entity, opening trade accounts that report payment activity, and paying your bills on time consistently.

Get on-demand access to business credit reports without a long-term commitment. Schedule a free consultation with Command Credit to see how flexible business credit reporting supports smarter risk and credit decisions.