If you were to describe today’s economic landscape in one word, many C-suite executives would call it volatile. Inflation, interest rates, costs, supply shocks, labor shortages — there’s a lot at play here. Many sectors are struggling, and some are closing completely. Business bankruptcies increased by double digits in the last half of 2024 and the first half of 2025. Closings left behind more than $30 billion in unpaid bills.

Financial risk management must account for all of this and more.

At the same time, digital payments have accelerated revenue cycles and also opened doors to sophisticated fraud. While it’s impossible to eliminate all risk, you can implement business intelligence tools to detect risk more quickly and clearly, act decisively, and turn uncertainty into an advantage.

Command Credit supports this shift by providing the actionable data you need, including business credit reports, account monitoring, background investigations, and portfolio monitoring. This gives you the context you need to make better decisions and catch warning signs earlier.

What Is Credit Risk Assessment?

Credit risk assessment is the process of evaluating the likelihood that your customers, suppliers, or partners will default or delay payments. You are trying to answer three questions here:

- Do they have the means to pay?

- Will they pay?

- What’s the impact if they do not pay?

When you can answer these questions, you mitigate risk.

The strongest assessments bring multiple data streams together, such as:

- Financial statements that reveal capital structure and liquidity.

- Credit bureau data showing credit limits, score trends, and derogatory marks.

- Trade payment histories that expose real behavior across vendors.

- Credit lines and utilization showing flexibility during downturns.

When combined, these inputs create a foundation for financial data analysis and pave the way for you to accurately evaluate risk whether you’re considering granting credit, monitoring accounts, or evaluating your entire credit portfolio.

Command Credit’s business credit reports and portfolio management give executives on-demand visibility into creditworthiness and exposure across accounts. With a few clicks, you can see score movements, new filings, or days beyond terms (DBTs). This is actionable data you can use in your business risk assessment.

Here’s how this might play out. A manufacturer monitoring supplier accounts might notice suppliers suddenly falling behind in paying their bills and getting close to maxing out their credit line. Because the manufacturer sees these warning signs, it can take action proactively. It might increase safety stock or start sourcing backup suppliers just in case. So, if a supplier is unable to deliver, the manufacturer is not left without the materials they need to serve their customers.

Why Risk Management Is Important for Executives

Risk management isn’t a back-office chore. It’s a boardroom responsibility tied directly to shareholder value.

Cash surprises trigger earnings surprises. Vendor failures ripple into missed commitments. Controls that capture fraud after settlement are costlier than controls that prevent it before authorization. And the risk is nearly unavoidable. Nearly 80% of organizations fell victim to payment fraud attacks last year. That figure illustrates a core truth these days. Fraud is no longer an edge case.

It’s commonplace. Fraud prevention requires cross-functional discipline from finance, operations, IT, and compliance.

Executive accountability starts with forward-looking visibility both externally (customers, suppliers, counterparties) and internally (cash conversion cycles, AR aging, payment approvals, etc.). Robust financial risk management helps leaders to:

- Protect working capital by aligning terms and limits with real risk.

- Maintain vendor reliability by spotting signs of distress before it becomes a disruption.

- Improve forecasting accuracy by replacing static assumptions with live indicators.

- Support sustainable growth by pricing, underwriting, and sourcing with discipline.

How Do You Identify Financial Risks?

The first step in business risk assessment is knowing where risk hides. You will find it in customers who stretch terms, suppliers whose cash burn accelerates, transactions that don’t fit expected patterns, and processes that allow exceptions without approval.

Four main categories cover most of what matters:

- Credit risk: default or late payments that hurt your cash flow.

- Supplier risk: insolvency, non-performance, or quality failures.

- Fraud risk: Scams such as invoice fraud or faking business data.

- Operational risk: data, process, or compliance failures that allow errors.

Conditions are worsening in some sectors. The American Bankers Association is reporting a significant drop in business credit quality in 2025. That softening raises both the likelihood and the impact of delinquency.

Financial data analysis needs to blend both internal and external signals, what we call outside-in and inside-out metrics, to get actionable data from your business intelligence tools:

- Outside-in: credit bureau scores, lien/collection filings, and trade data.

- Inside-out: payment histories, returns, disputes, and order patterns.

Your customer and vendor risk management should start at onboarding, with a rigorous evaluation of creditworthiness and financial health, and adjust terms and limits based on that profile.

How Do You Create a Risk Management Framework?

A risk management framework is the operating system for your defenses. It’s the way you identify, measure, monitor, and respond to threats using data and governance. A practical C-suite framework looks like this:

- Identify risks using credit, payment, and operational data.

- Quantify exposure through scoring models and predictive analytics.

- Monitor continuously with real-time dashboards and alerts.

- Respond proactively with scenario planning and mitigation actions.

This only works, however, if you have up-to-date and accurate data and strong internal policies that you apply consistently.

What Is Credit Portfolio Management?

Credit portfolio management gives executives a holistic view of exposure across customers, partners, and vendors. Instead of treating accounts in isolation, you see correlations and concentrations: which industries dominate your AR, which regions share economic risk, which suppliers form single points of failure.

Portfolio thinking moves beyond single-account risk to systematic risk. The objective is balance, pursuing growth with high-value relationships while diversifying enough to absorb shocks.

It’s become a bigger issue; 81% of businesses say they’re seeing increases in delayed payments. In turn, more than half of U.S. companies are now paying their suppliers late as of July 2025, citing cash flow issues. This can create a ripple effect that impacts everyone in the supply chain.

Your financial data analysis must include account, portfolio, and vendor risk management.

Using Business Intelligence Tools for Better Decisions

Business intelligence tools can translate data into actionable insights, tracking payment trends to uncover potential problems and helping with fraud prevention strategies.

Executives increasingly rely on dashboards that integrate AR, AP, and credit data to visualize payment trends, detect anomalies, and sequence interventions. The data provides the insight you need to know to:

- Communicate with clients and suppliers before their financial issues hurt your business.

- Adjust credit limits when score momentum turns negative.

- Reallocate resources toward sectors with stronger payment reliability.

- Prioritize customers by lifetime value adjusted for risk, not revenue alone.

Fraud Prevention and Vendor Risk Management

Fraud is on the rise. AI tools have made it easier to fake identities, invoices, and scam businesses into paying. Fraud losses now top $40 billion globally. The Association of Certified Fraud Examiners (ACFE) estimates that companies lost as much as 5% of revenue to fraud each year.

Credit, identity, and behavioral data help detect anomalies early. Common risk signals include:

- Mismatched tax IDs or bank details

- Duplicate billing

- Fraudulent billing

- Significant number of change orders

- Unclear ownership details

One of the biggest warning signs is when a company or supplier’s financial health starts to deteriorate. When they start paying bills late, max out credit lines, or hint at bankruptcy, you need to monitor things closely. While it doesn’t mean fraud is going to happen, these conditions are often precursors to those who do commit fraud out of desperation.

You need to do your due diligence when onboarding clients and suppliers, along with continuous monitoring of client and vendor risk management factors to safeguard your business. Integrating vendor and customer data into the same vetting and monitoring process produces a unified risk perspective. When a supplier’s credit tightens and their delivery lead times slip simultaneously, the pattern might indicate potential problems. When a customer’s payment behavior slows while their order volume spikes, it may indicate channel stuffing or potential fraud. Seeing both sides together gives you the evidence to act appropriately.

Operationalizing the Framework: Governance, Metrics, and Cadence

Building a robust financial risk management require you to set up your system to monitor the key metrics to ensure risk doesn’t exceed your acceptable threshold. These metrics might include:

- Delinquency rates

- Risk scores by segment

- Supplier on-time/in-full deliveries

- Chargeback or dispute trends

- Alert volume above certain thresholds

Your credit and ordering policies should use these metrics when making credit or purchasing decisions. When you see warning signs, you can justify decisions to change terms, reduce credit limits, or look for alternative suppliers.

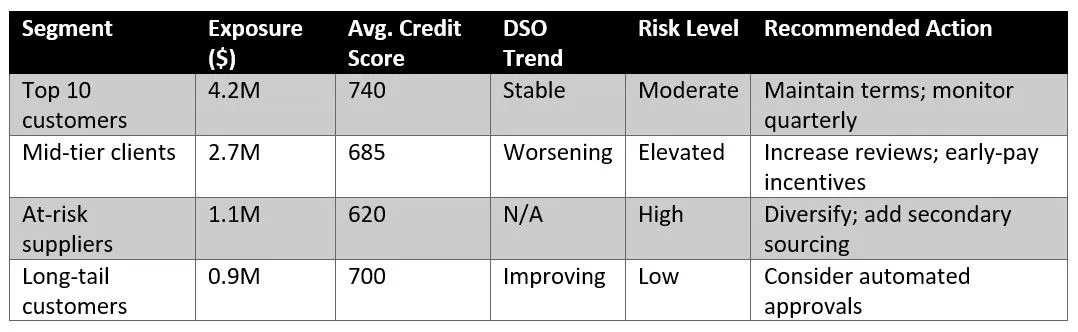

Your policies should be transparent and applied consistently across your portfolio. While your strategy might look completely different, here’s an example of how you might approach your credit risk assessment, and actions to take by segmenting your risk.

And here’s how this might play out in the real world. A company using Command Credit’s portfolio monitoring to flag warning signs might see increasing exposure in a particular segment or industry. By examining changes in credit scores, transactional behavior, and weighing overall exposure, the company can act according to their policies.

Linking Risk to Strategy and Capital Allocation

Senior leaders can take business risk intelligence one step further by embedding it into planning cycles. As part of your financial risk management strategy, you can use portfolio reviews to plan targeted sales outreach, pricing and discounts, incentives for early payment, and supplier sourcing.

For example, you might decide to prioritize expansion in sectors with strong credit momentum and cut back on exposure in segments where score deterioration and DSO slippage move together. In capital planning, you can also prioritize working capital, like early-pay discounts and dynamic terms, that your data shows produce the highest cash yield per dollar.

Risk intelligence can produce actionable insight for who to do business with and how you approach business with them.

Risk Intelligence as a Leadership Advantage

With credit, vendor, and fraud data, you get the insight you need to make better business decisions and protect your bottom line. The key, however, is operationalizing this intelligence. Leading companies apply three specific strategies:

- Stabilizing cash flow: Aligning terms and exposure to counterparty quality.

- Hardening supply chains: Validating and diversifying suppliers that are core to your business.

- Reducing fraud: Preventing bad transactions ahead of time rather than after-the-fact.

Command Credit’s value proposition maps directly to those outcomes: credit intelligence from multiple credit bureaus, account monitoring, portfolio monitoring, and background investigations when necessary.

FAQs — Frequently Asked Questions About Financial Risk Management

What is financial risk management? Financial risk management is the process of identifying, measuring, and mitigating potential financial losses arising from credit defaults, market volatility, fraud, or liquidity constraints.

How do you measure business risk? Business risk is measured through quantitative models, such as credit scoring, probability-of-default analysis, portfolio exposure ratios, and qualitative assessments of vendor, industry, and operational factors.

What is payment risk? Payment risk is the likelihood that a customer or business partner will delay or fail to make payments, affecting your cash flow.

What is credit risk modeling? Credit risk modeling uses statistical and AI tools to predict the probability of default or delinquency, helping you make data-driven decisions about credit and suppliers.

For organizations seeking deeper visibility and control across credit, fraud, and vendor risks, Command Credit delivers enterprise-grade data and analytics to help you make better, smarter business decisions. Schedule a free consultation today.