According to the Federal Reserve's Small Business Credit Survey, nearly 70% of small employer firms have used personal funds to support their businesses, and the latest report showed that nearly 40% of companies have debt topping $100,000. That’s a lot of risk, with outstanding debt today higher than in 2000.

With so much on the line, determining creditworthiness is more important than ever, and it’s no longer strictly a math problem. It’s also a matter of interpretation, context, and insight. That’s why credit teams increasingly rely on both quantitative and qualitative methods to form a complete picture of risk.

Each approach brings unique strengths.

Quantitative risk analysis provides the hard data (loss projections, probabilities of default, benchmark scores) while qualitative risk analysis offers the nuance needed to evaluate situations where data alone falls short.

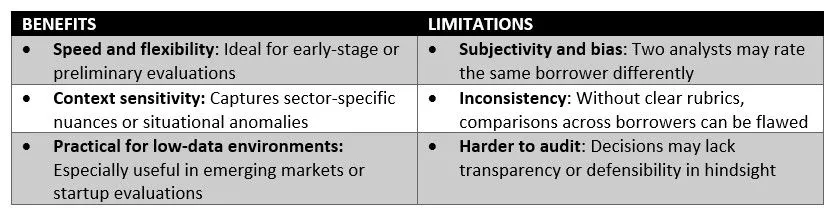

Qualitative Risk Analysis

Qualitative risk analysis is an experience-driven, subjective method of evaluating credit risk. Rather than producing numeric probabilities or dollar values, this approach assesses risk factors using descriptive terms such as “low,” “moderate,” or “high.” This relies on expertise and historical data to identify risks that may not be revealed by traditional models.

As an example, a seasoned analyst may flag a company’s rapid executive turnover as a concern even if its payment history looks fine on paper.

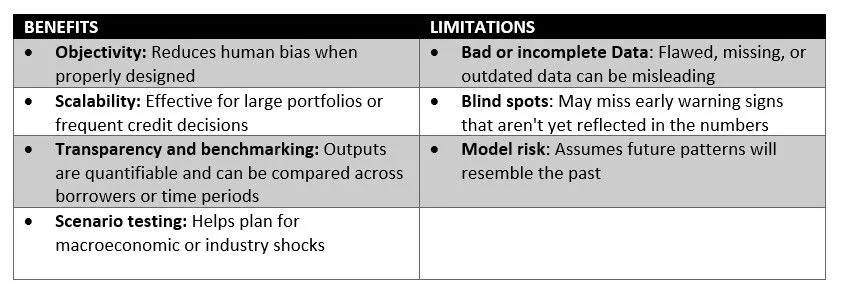

Quantitative Risk Analysis

Quantitative risk analysis utilizes statistical models and historical data to assign numerical values to risk. This includes calculating and predicting default, estimating potential losses, and running simulations to understand various scenarios.

Credit scoring systems, loan underwriting software, and portfolio risk assessments lean heavily on data and machine learning algorithms to provide credit risk scores.

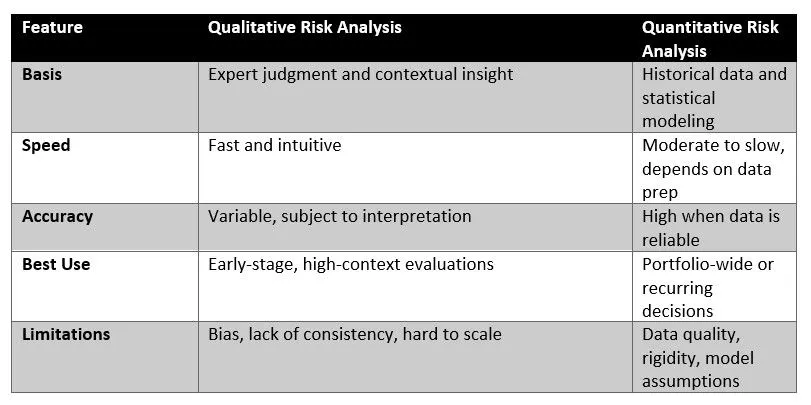

Quantitative vs Qualitative: A Side-by-Side Comparison

Here’s how the two approaches stack up side-by-side.

When to Use Each Method in Credit Risk Management

There’s no one-size-fits-all strategy in credit risk analysis. Each method shines in different scenarios:

Startup vendor with no payment history?

Qualitative methods give insight into management quality, business model viability, and external risks.

Reviewing a large supplier base?

Quantitative tools streamline screening with consistent metrics across thousands of records.

Assessing a borrower entering a distressed industry?

Combine both: let your model flag numeric concerns and use qualitative judgment to evaluate resilience factors.

The best credit teams adopt a layered approach. Qualitative analysis adds narrative context and catches red flags early, while quantitative analysis provides the statistical backbone for confident forecasting and regulatory compliance.

Building Your Hybrid Risk Strategy

Forward-thinking credit professionals are integrating both methods into unified workflows. This improves credit decision quality and compliance.

Common approaches include:

- Blended credit scoring models: Merge numerical inputs with qualitative overrides or analyst weightings.

- Two-tier risk assessments: Use quantitative filters for initial screening, then apply qualitative reviews to refine risk tiers.

- Integrated dashboards: Centralize both numeric and narrative data in a single risk management platform.

Keep in mind that however you approach credit risk management, independent data sources are essential. Avoiding reliance on a single credit bureau or score also helps you mitigate concentration risk.

Adopting a Hybrid Approach to Credit Risk Management

Quantitative risk analysis delivers precision and consistency, while qualitative risk analysis offers the adaptability and insight to respond to new threats. Together, they form a more resilient framework to help you make better credit decisions.

Strengthen your credit risk decisions with business credit reports and credit scores from multiple reporting agencies to produce data-driven insights that complement professional judgment. Request a consultation today to discuss your credit risk data needs.