Corporate credit risk management in 2025 is anything but routine. While many foundational principles remain, today’s risk professionals must contend with increasingly complex credit structures, economic volatility, and rising expectations for real-time insight.

Companies are sharpening their corporate credit risk management framework in light of increasing default risk, which has grown to 9.2% according to Moody’s, the highest mark since the financial crisis back in 2008.

In this environment, credit teams need more than basic scoring models. They need flexible credit risk management frameworks, better data, and advanced techniques that allow them to evaluate risk at both macro and micro levels. Still, the majority of credit risk managers report that data quality remains their biggest constraint.

So, let’s explore the essential components of a modern credit risk management framework, along with advanced strategies that help minimize credit risk.

What Sets Corporate Credit Risk Apart

Corporate credit risk isn’t just about numbers on a report. It involves assessing layered entities, evaluating strategic dependencies, and making judgment calls about long-term viability. Where small business risk can often be quantified through standardized scores, corporate risk frequently demands deeper insight.

Key differentiators include:

- Larger exposure per account, with higher potential loss

- Complex corporate structures, multiple decision-makers, and interdependent legal entities

- Significant impact of qualitative factors: market position, governance, concentration risk

- Cross-border considerations. including currency risk, regulatory differences, and enforcement limitations

In short, corporate credit risk calls for a more strategic, multi-dimensional approach.

Core Elements of a Corporate Credit Risk Management Framework

There are a few core elements that make up a solid framework.

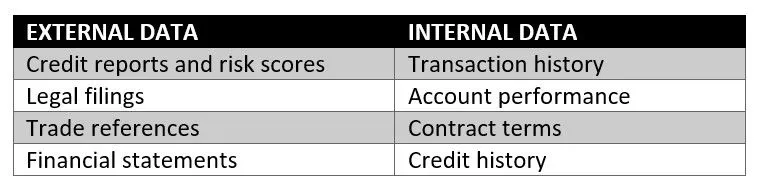

Risk Identification and Data Collection

Strong risk frameworks begin with comprehensive data. Corporate credit teams typically collect both internal and external inputs.

Using multiple data providers is key. Discrepancies between bureaus like Experian, Equifax, and D&B often reveal hidden risks. Third-party platforms like Command Credit allow teams to access multiple sources on demand, without being locked into a single bureau.

Quantitative Risk Scoring

Quantitative scoring remains a backbone of corporate credit risk management, but it must be calibrated to corporate contexts. Common tools include probability of default models and financial ratio analysis, such as leverage ratios, current ratios, and the Altman Z-score. Scores should also incorporate payment behavior data, Days Beyond Terms (DBT), UCC filings, and bankruptcy records. The goal is to create a structured numerical view of each entity’s creditworthiness while leaving room for qualitative interpretation.

Qualitative Overlays

Data can tell you what happened but not always uncover the why. Qualitative overlays allow you to assess intangible factors such as executive turnover, pending litigation, or sector volatility. By digging into the logic behind the data, you can often prioritize risk for intervention.

Risk Segmentation and Exposure Limits

Risk segmentation also helps here. Grouping clients by risk tier, industry, geography, or strategic importance can provide guidance on where attention is needed. This might mean lower credit limits, cash upfront, shorter terms, or stricter monitoring requirements.

Segmentation also helps senior leadership visualize the company’s total exposure and risk concentration.

Monitoring and Triggers

An effective credit risk management framework includes mechanisms to flag risk changes before they become problems. Monitoring can be tied to events, such as a new UCC filing, delinquent payment, or a decline in DBT scores. Other triggers may include behavioral changes, high credit utilization, or other custom terms.

Modern credit teams are incorporating real-time monitoring services into their workflows, allowing for earlier interventions and fewer surprises.

Advanced Techniques for Corporate Credit Risk Management

Today’s risk teams must plan not only for what’s happening now but also for what might happen in the future. Scenario modeling allows you to simulate the impact of economic shocks, interest rate changes, or customer defaults on your cash flow. In particular, stress testing helps quantify how risk might spread across your portfolio.

Whether you are adjusting exposure to a single client or refining reserve strategies, scenario-based modeling helps you forecast the future and not just report on the past.

Blended Risk Scoring Models

A growing number of credit teams are using blended scoring systems, integrating internal performance data with third-party credit signals. For example, invoice aging patterns and contract utilization can be layered alongside external credit scores to yield a more accurate, context-aware risk rating.

Weighting can be adjusted by account size, industry, or strategic value. This allows you to move beyond static scoring and make decisions that reflect both history and current behavior.

Multi-Entity and Cross-Border Risk Structuring

Many corporate accounts involve complex legal arrangements. This might include subsidiaries, joint ventures, or multi-entity guarantees. Evaluating credit risk across these structures can be challenging.

Credit professionals must assess the strength of guarantees, review parent-subsidiary relationships, and understand enforcement rights across borders. Working with providers who support international data access can significantly improve your risk assessments.

Building a Flexible Framework

Corporate credit teams need a framework that is both structured and adaptable. Economic conditions can shift rapidly, and risk policies need to adjust without rebuilding systems from scratch.

A flexible framework includes:

- Modular evaluation steps that scale with account size or complexity

- Integration of on-demand data sources for real-time insight

- Clear documentation of scoring logic, overrides, and review cycles

- Ongoing training to align credit, sales, and finance teams around consistent policy enforcement

With these elements in place, you can manage credit risk more proactively while supporting commercial agility.

Enhance your corporate credit risk management framework with Command Credit’s multi-bureau credit reports and on-demand assessments. Get the data you need, when you need it, without a long-term subscription.