In business, you take calculated risks all the time. Whether it’s hiring someone, taking on debt or investors, creating new product lines, or opening the door every morning. There’s always some level of risk, which is why nearly 600,000 businesses close each year.

However, there are steps you can take to protect yourself and your cash flow. Checking business credit reports can help you evaluate the financial health of your customers, clients, and partners to make better decisions about offering business credit.

You cannot mitigate all risks. Natural disasters, supply chain disruptions, global unrest, and pandemics can cause significant problems. But you can mitigate your risk when granting credit. In this guide, we will explain the benefits of risk management, how to check a business credit report, and the different types of business credit reports you can get.

Benefits of Checking a Business Credit Report

There are several key benefits to pulling business credit reports. Here are some of the key use cases.

Mitigating Credit Risks

Armed with comprehensive information about a business's financial well-being, you can make informed decisions regarding granting credit, credit limits, and lending terms. This proactive approach helps you mitigate risks and financial losses.

Assessing Potential Partnerships

Business credit reports are invaluable tools when you are evaluating prospective partners or suppliers. By reviewing their credit histories, you can gain confidence in their ability to fulfill obligations.

Evaluating Credit for New Business

When new enterprises emerge, they often have limited credit histories. Examining their business credit reports can offer you insights into the individuals behind the ventures and their credibility. Additionally, these reports can help you verify business identities, safeguarding against potential impersonation fraud.

Monitoring Existing Relationships

Even long-standing clients or customers can experience financial upheavals. Regularly pulling credit reports on your current accounts provides an early warning system, allowing you to detect changes in creditworthiness before delinquencies occur.

Gaining a Competitive Edge

By evaluating the financial health of your competitors or potential acquisition targets through their credit reports, you can acquire valuable competitive intelligence. This information can enhance your strategic decision-making and provide a competitive advantage.

Checking Suppliers

You may want to consider pulling business credit reports for your suppliers, especially when you are doing business for the first time. If you are depending on a supplier to provide you with raw materials, goods, or services and they are unable to do so because of finances, you are putting your business and revenue at risk.

Enhancing Your Credit Management

Reviewing your own business credit report is a good idea, too. Understanding how others perceive your company's financial standing can be crucial when you're seeking loans or credit from other businesses. This knowledge can aid you in negotiating favorable rates and terms, especially for small business owners.

Checking for Accuracy

You should check your business credit report occasionally to make sure it is accurate. Mistakes do happen, so checking can help you find anything wrong.

You can dispute information on credit reports through each of the credit reporting agencies. They will generally resolve complaints quickly as they want the reports to be accurate. The more information you provide, the easier it will be to get information corrected. Most of the time, mistakes are minor, such as the wrong business address. However, even small mistakes may cause problems when someone else wants to view your credit report.

However, there is no federal law that outlines the processes or protections for businesses when it comes to credit reporting—unlike consumer protections in the Fair Credit Reporting Act. The Federal Trade Commission (FTC) is currently reviewing five credit reporting agencies to ensure they are fair and responding to complaints.

What Do Business Credit Scores Show?

Business credit scores are compiled by credit reporting agencies based on a company’s financial data and credit history in much the same way as a personal credit score is created. The credit agencies will review several key factors including:

- Length of credit history

- Credit utilization

- Payment history

- Public records

This produces an overall score that can help you determine whether a customer or client is a good credit risk.

What Is a Good Credit Score for Business Credit?

While personal credit scores generally fall on a scale of 300 to 850, business credit scores typically range from one to 100 with higher scores indicating lower risk. However, there are several types of risk measurements you can get depending on which credit reporting agency you use for your business credit report.

Looking at basic credit scores, if you are wondering, “Is 64 a good business credit score?” (for example), the answer will generally be “No.” Most lending companies typically want to see a score in the 75+ range before they approve loans.

In general:

- Scores 0–49 are considered severe risk.

- Scores between 50 and 59 are considered high risk.

- Scores between 60 and 79 are considered moderate risk.

- Scores above 80 are considered low risk.

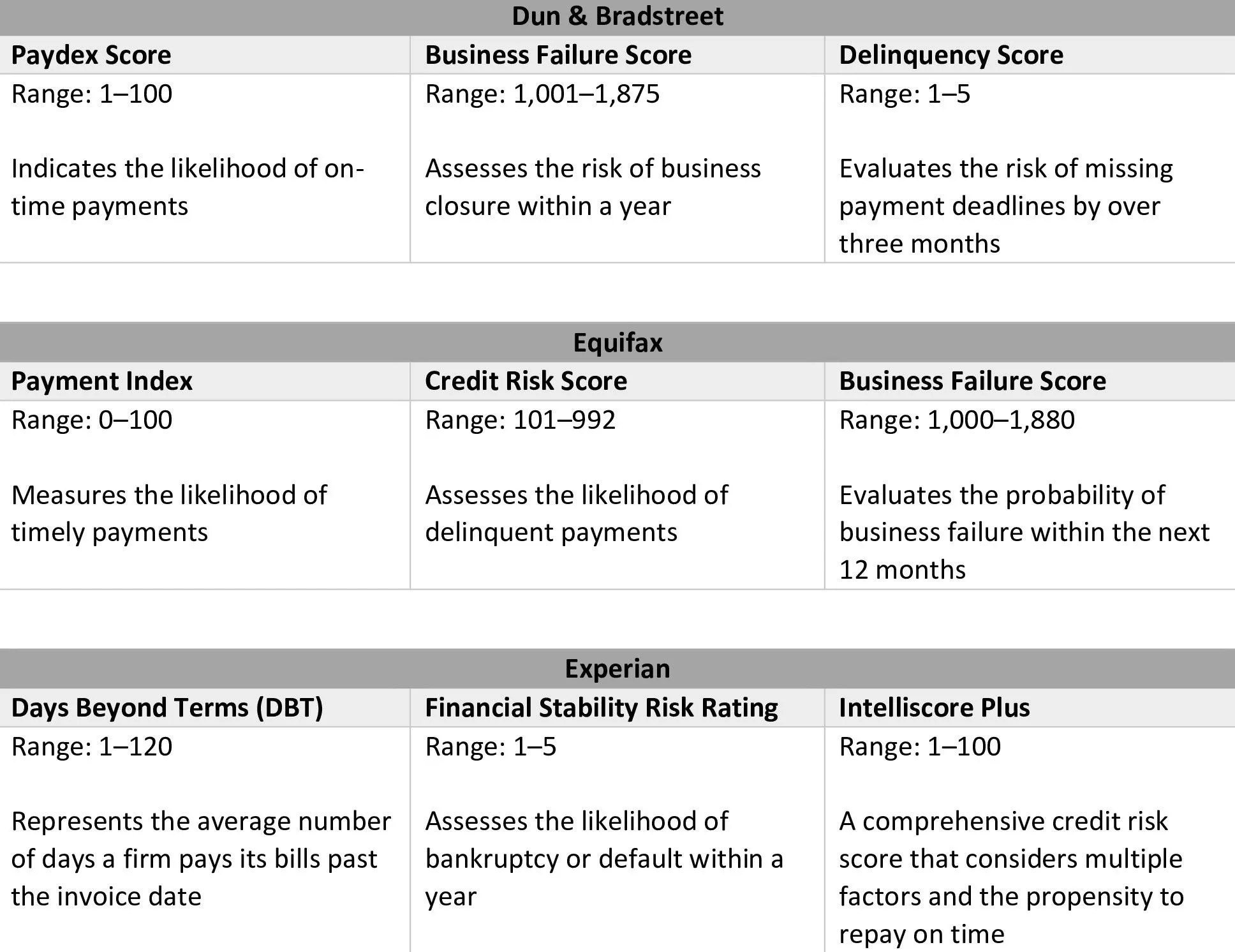

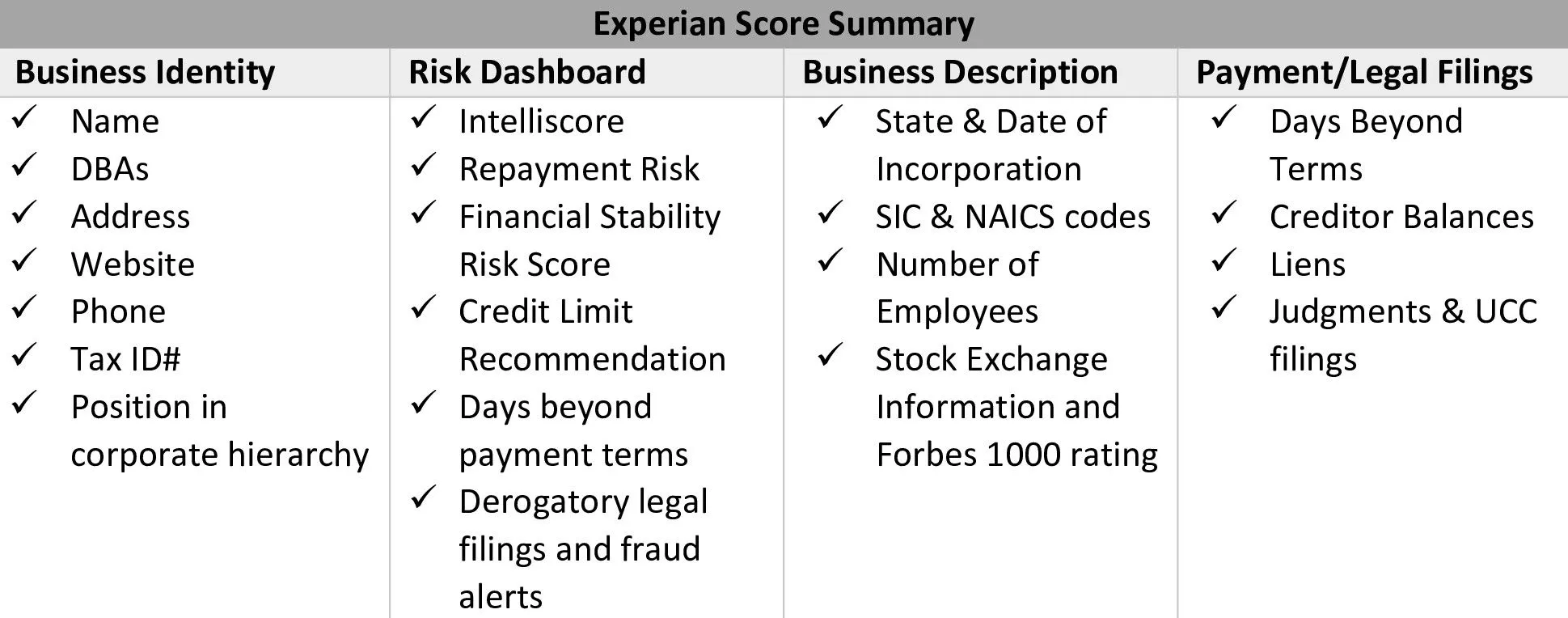

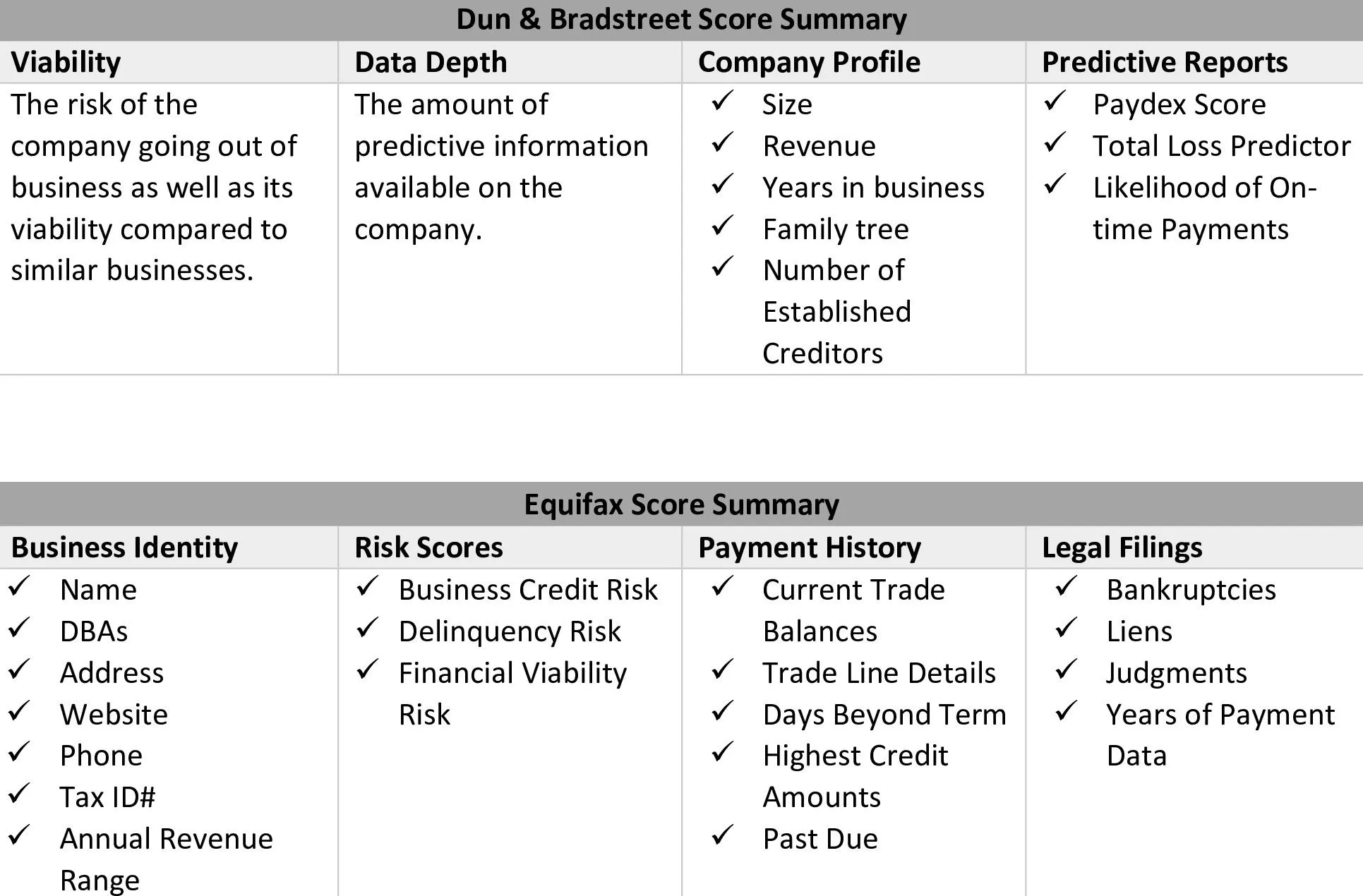

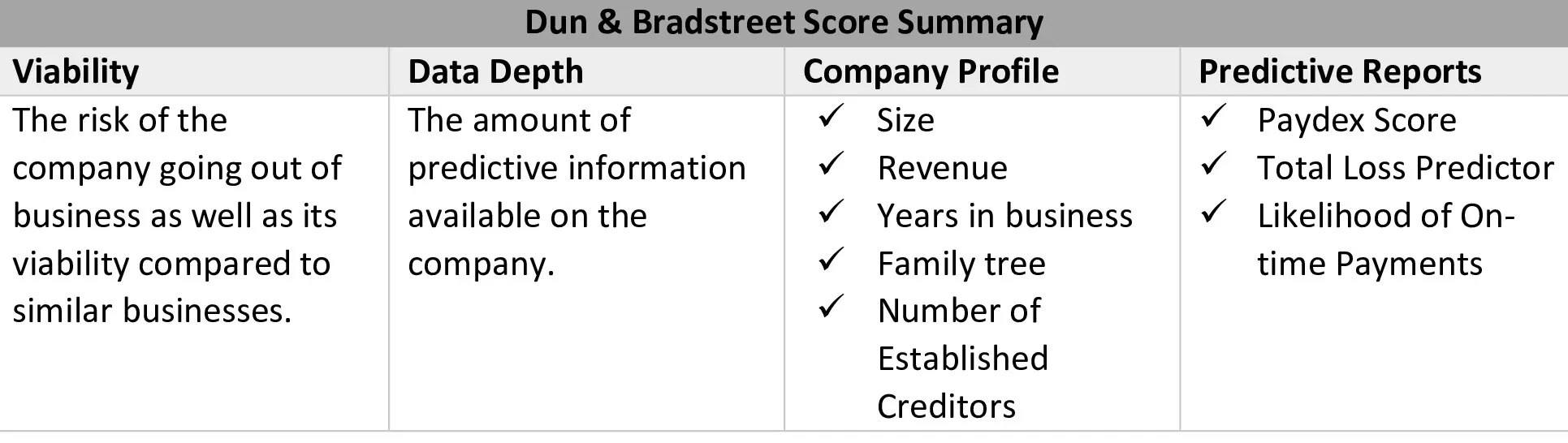

Which Is the Best Business Credit Report for Your Business?

The best business credit report for your business will be the one that provides the information you need to make the best decisions for you, based on your credit requirements and risk tolerance. Each of the three different credit reporting agencies uses slightly different information and reports things differently, so you will want to compare them carefully and view samples to make sure you get what you need.

Here is an overview of what you get from Experian, Equifax, and Dun & Bradstreet business credit reports.

View samples of Experian business credit reports.

View samples of Dun & Bradstreet business credit reports.

View samples of Equifax business credit reports.

As you can see, there are some similarities but also some marked differences. There are also different types of business credit reports from these credit reporting agencies as well. If you are unsure which is right for you, you can give us a call at Command Credit, and we can discuss your options.

What Are the Most Important Things to Look at?

Start with the business credit score. While there are no guarantees, someone with a solid financial track record is much more likely to pay their bills on time. Keep an eye out for changes that could signal a deteriorating financial position.

Credit Utilization

If a business is starting to max out its available credit, it can be a warning sign that they are overextended. Consistently bumping up against maximum utilization can be a red flag that a business is having difficulty managing its finances and paying its bills.

Days Beyond Terms (DBT)

DBT reports how many days on average a business pays its bills past the due date. When you see the days beyond term start to increase, it’s another warning. Monitoring this metric can help you be proactive about collections before an account goes delinquent or into default.

Legal Filings

Legal issues can also increase credit risk. Besides bankruptcies, you want to watch out for liens against property or judgments that may hurt a company’s ability to pay its bills promptly.

SIC and NAICS Industry Codes

One of the other things you will see on a credit report for business is the SIC or NAICS industry codes. Standard Industrial Classification (SIC) and North American Industrial Classification System (NAICS) identify a company’s primary business—which may not always be obvious from its name. This helps you see whether someone is in what’s considered a high-risk business, such as auto and boat dealers, travel agencies, auto repair, or cash-intensive businesses, such as retailers, gas stations with convenience stores, restaurants, and beer/wine/liquor stores.

NAICS publishes a full list of what it considers high-risk and cash-intensive businesses based on analysis.

How Do I Pull a Credit Report for Business?

The easiest way to pull a business credit report is to use Command Credit. We do not require you to sign up for a subscription or commit to any monthly or minimum use. You can sign up for a free account and then pull as many or as few credit reports as you want.

It really is easy. Just enter the name of the business and a few basic details, pay online, and you can pull the report instantly with no waiting. You can choose from Experian, Equifax, or Dun & Bradstreet—or all of them if you want. For international businesses, you can also get business credit reports from our partners at Credit Reports World.

Frequently Asked Questions — FAQs

Are business credit scores public? Can anyone pull a business credit report?

While business credit scores are not public, anyone can pull a report. Unlike personal credit reports, you do not need permission before accessing a business credit report.

What does the B mean on a credit report?

If you see a “B” on a credit report, it means there has been a bankruptcy.

What credit score does an LLC start with?

When a limited liability company (LLC) first starts, it typically does not have an established credit history or score. The credit reporting agencies do not automatically assign credit scores for newly formed businesses.

What is a good credit score for an LLC?

A good credit score for an LLC is the same as any other business. A score between 60 and 79 is considered a medium credit risk. Scores above 80 are considered low risk.

With Command Credit, you can pull business credit reports from Dun & Bradstreet, Equifax, Experian, and Credit Reports World. Pull reports instantly without a subscription. Contact Command Credit today to get started.